It’s nearly two years since the Reserve Bank of Australia last changed interest rates – when it cut rates to a record low of 1.5% in August 2016. That’s a record period of inaction – or boredom for those who like to see action on rates whether it’s up or down. Of course, there are lots of views out that the RBA should be doing this or that – often held and expressed extremely – and so it’s natural that such views occasionally get an airing. This is particularly so when the RBA itself is not doing anything on the rate front.

And so it’s been this week with a former RBA Board member arguing that the RBA should raise rates by 0.25% to prepare households for higher global interest rates and that the RBA should consider ditching its inflation target in favour of targeting nominal growth.

Our view – rates on hold at least out to 2020

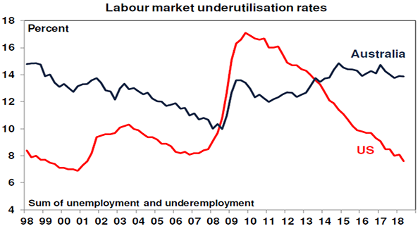

Our view for some time is that the RBA won’t raise interest rates until 2020 at the earliest. In terms of growth, a brightening outlook for mining investment, strengthening non-mining investment, booming infrastructure spending and strong growth in export volumes are all positive but are likely to be offset by topping dwelling investment and constrained consumer spending. As a result, growth is likely to average around 2.5-3% which is below RBA expectations for growth to move up to 3.25%. This in turn means that spare capacity in the economy will remain high – notably unemployment and underemployment at 13.9% – which will keep wages growth low and inflation down. On top of this house prices likely have more downside in Sydney and Melbourne over the next two years, banks are tightening lending standards which is resulting in a defacto monetary tightening and the risks of a US-driven trade war are posing downside risks to the global growth outlook. As such we remain of the view that a rate hike is unlikely before 2020 at the earliest and can’t rule out the next move being a cut.

Raising rates to prepare for higher rates makes no sense…

Against this backdrop, raising rates just to prepare households for higher global rates would be a major policy mistake:

-

It would be like shooting yourself in the foot so you can practice going to hospital. Some might argue that given high household debt you might miss the foot and hit something more serious – but I wouldn’t go that far!

-

What’s more it’s not entirely certain that outside the US higher global rates are on the way any time soon – particularly given the risks around a global trade war, the European Central Bank looks unlikely to be raising rates until 2020 and with Japanese inflation falling again a Bank of Japan rate hike looks years away.

-

The RBA needs to set Australian interest rates for Australian conditions not on the basis of other global economies that are in different stages in the cycle – notably the US which has unemployment and underemployment of just 7.6% in contrast to Australia where it’s 13.9%.

Source: Bloomberg, AMP Capital

-

Raising rates when there is still high levels of labour market underutilisation, wages growth is weak and inflation is at the low end of the inflation target would just reinforce low inflation expectations – causing businesses and households to question whether the RBA really wants to get inflation and wage growth back up to be more consistent with the inflation target and run the risk of a slide into deflation next time there is an economic slowdown.

-

The RBA has already provided numerous warnings that sooner or later rates will go up, effectively helping to prepare households that such a move may come and in recent times banks have raised some mortgage rates, albeit only slightly. Last year’s bank rate rises were in response to regulatory pressure and recently they have been in response to higher short-term money market funding costs as the gap between bank bill rates and the expected RBA cash rate has blown out by around 0.35% relative to normal levels. This has further reminded households of the risk of higher interest rates.

…nor does changing the inflation target

Suggestions to change the inflation target or move to some other target for the RBA get wheeled out every time we run above or below the target for a while but its served Australia well. When it’s above for a while like prior to the Global Financial Crisis some wanted to raise it, when it’s below for a while some want to cut it. And there are regular calls to move to something else like nominal growth targeting. But the case to change the target is poor:

-

The 2-3% inflation target interpreted as to be achieved over time has served Australia well. It’s low enough to mean low inflation, it’s high enough to allow for the tendency of the measured inflation rate to exceed actual inflation (because the statistician tends to understate quality improvement) and to provide a bit of a buffer before hitting deflation. And the achievement of it over time means the RBA does not have to make knee-jerk moves in response to under or overshoots because it can take time to get back to target.

-

Shifting to a nominal GDP or national income growth target would be very hard for Australia for the simple reason that nominal growth in the economy moves all over the place given swings in the terms of trade which the RBA has no control off. It would have meant much tighter monetary policy into 2011 than was the case and even easier monetary policy a few years ago when the terms of trade fell. In short it would mean extreme volatility in RBA interest rates.

-

And in any case, nominal GDP or income growth is made up of two different things – inflation and real growth – so targeting just the aggregate could lead to crazy results for example if the target is 4.5% the RBA could get 4.5% inflation and say it hit its target! Which would be nuts.

-

Finally, while low rates risk inflating asset price bubbles it’s worth noting that apart from Sydney and Melbourne home prices, the period of low rates has not really led to a generalised asset price bubble problem in Australia. And in any case as we have seen recently in relation to Sydney and Melbourne property prices – which are now falling (despite still ultra-low interest rates!) – the asset price problem where it does arise can be dealt with via macro prudential controls on lenders. Arguably, if we had moved faster on the macro prudential front around 2014-2016 then the east coast housing markets would have been brought under control earlier and rates could have come down faster in Australia and we could now be in a tightening cycle…but that’s all academic!

Bottom line

The bottom line is that the RBA should stick to its inflation target and ignore those arguing for a premature rate hike. Our assessment is that this is just what it will do and that rates will be on hold for a long while yet. In the meantime, the debate about rates will no doubt rage on.

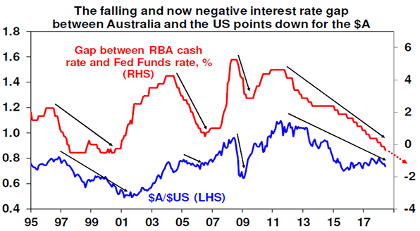

Continuing low interest rates in Australia will mean term deposit rates will stay low, search for yield activity will still help yield-sensitive unlisted investments like commercial property and infrastructure (albeit it’s waning) and an on-hold RBA with a tightening Fed is likely to mean ongoing downward pressure on the Australian dollar as the interest rate differential goes further into negative territory.

Source: Bloomberg, AMP Capital

While a crash in the $A may concern the RBA, we saw in both 2001 when it fell to $US0.48 and 2008 when it fell from $US0.98 to $US0.60 in just a few months that the inflationary consequences of a lower $A are not what they used to be and in any case the RBA would likely welcome a fall to around $US0.65-0.70.

Source: AMP Capital 28 June 2018

Author: Dr Shane Oliver, Head of Investment Strategy and Chief Economist, AMP Capital

Important note: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.